Investing has never been more accessible than it is today. Whether you’re opening your very first investment account or building a retirement portfolio, you’ll likely come across three terms repeatedly: ETF vs mutual fund vs index fund. At first glance, they seem almost identical because all three allow investors to own a diversified basket of investments rather than purchasing individual stocks or bonds. However, their structure, management style, costs, taxation, and trading methods differ significantly. Understanding these differences is essential because choosing the wrong investment vehicle could mean paying higher fees, facing unnecessary taxes, or investing in a product that doesn’t align with your financial goals. According to recent industry data, indexed mutual funds and ETFs collectively now hold more assets than actively managed funds in several major markets, reflecting the growing popularity of low-cost passive investing.

If you’ve searched for ETF vs mutual fund vs index fund, you’re probably wondering which option offers the best balance of growth, risk, and flexibility. The answer isn’t as straightforward as choosing one over the others because each serves a different purpose. Some investors prioritize lower fees, while others prefer professional management or automatic investing. Understanding how these investment products work together—and sometimes overlap—will help you make informed decisions that fit your personal financial strategy. Throughout this guide, we’ll break down each investment type in simple language, compare their strengths and weaknesses, and explain when one may be a better choice than another.

Why Understanding Investment Funds Matters

Many beginner investors assume investing is all about picking the next winning stock. In reality, successful investing often comes down to consistency, diversification, and keeping costs low. Investment funds were created to simplify this process by pooling money from thousands—or even millions—of investors into professionally managed portfolios. Instead of researching dozens of individual companies, you gain exposure to hundreds or even thousands of securities through a single purchase.

Today’s financial markets also offer more choices than ever before. Exchange-Traded Funds (ETFs), actively managed mutual funds, and index funds continue to evolve with lower fees and broader market access. Industry reports published in 2026 show expense ratios remain near historic lows, making diversified investing more affordable for everyday investors than at any point in recent decades.

Understanding these products helps you:

- Choose investments that match your financial goals.

- Reduce unnecessary investment costs.

- Build a diversified portfolio with lower risk.

- Avoid common beginner investing mistakes.

- Create a long-term wealth-building strategy.

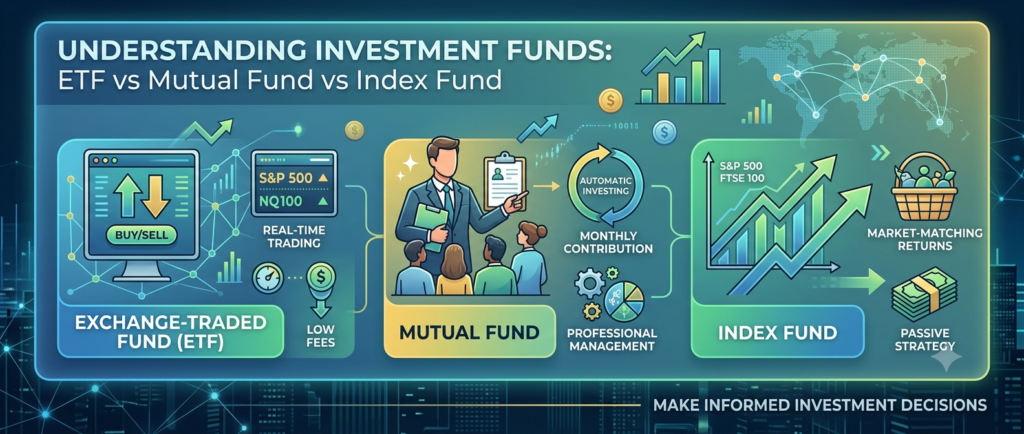

What Is an ETF?

An Exchange-Traded Fund, commonly called an ETF, is an investment fund that trades on a stock exchange just like individual company shares. When you buy an ETF, you’re purchasing a small ownership stake in a portfolio containing stocks, bonds, commodities, or other assets. Unlike traditional mutual funds, ETFs can be bought and sold throughout the trading day at market prices, giving investors flexibility similar to trading stocks.

How ETFs Work

Most ETFs are designed to track a market index such as the S&P 500, Nasdaq-100, or FTSE indices, although actively managed ETFs have become increasingly popular in recent years. Because ETFs generally follow predefined investment rules rather than relying heavily on fund managers, operating costs are often lower than actively managed funds. Investors can also monitor real-time prices throughout the day, making ETFs attractive for those who want greater control over buying and selling decisions.

Key Benefits of ETFs

Some of the biggest advantages include:

- Lower management fees

- Real-time trading during market hours

- Broad diversification

- High transparency

- Greater tax efficiency in many jurisdictions

- Availability across nearly every investment sector

For many long-term investors, ETFs provide a simple, low-cost way to build wealth while minimizing ongoing expenses.

What Is a Mutual Fund?

A mutual fund is one of the oldest and most widely used investment vehicles in the financial world. It pools money from thousands of investors and is managed by professional fund managers who decide which securities to buy or sell based on the fund’s investment objective. Unlike ETFs, mutual funds are priced only once each trading day after the market closes. This means every investor who buys or redeems shares during the day receives the same closing Net Asset Value (NAV). Mutual funds can invest in stocks, bonds, money market instruments, or a combination of assets, making them suitable for investors with different financial goals and risk tolerances. Many retirement accounts and employer-sponsored investment plans also rely heavily on mutual funds because of their accessibility and long-term investment focus.

Professional management is one of the biggest selling points of mutual funds. Investors who do not have the time or knowledge to research individual securities often appreciate having experienced portfolio managers make investment decisions on their behalf. However, this convenience usually comes with higher expense ratios compared to passively managed investment products. Actively managed mutual funds also aim to outperform market benchmarks, although research consistently shows that many struggle to beat broad market indexes over long periods after accounting for fees. That doesn’t mean mutual funds are a poor investment—they simply serve investors who value expert management and are willing to pay slightly higher costs in exchange for that service.

How Mutual Funds Operate

When you invest in a mutual fund, your money is combined with contributions from other investors. The fund manager uses this capital to purchase a diversified collection of securities based on the fund’s stated objectives. Whether the goal is growth, income, capital preservation, or balanced investing, each mutual fund follows a documented investment strategy. Since investors own shares of the fund rather than the underlying assets directly, gains or losses are shared proportionally among all shareholders.

One feature many investors appreciate is the ability to automate investments. Monthly contributions can be scheduled regardless of market conditions, helping investors build wealth through dollar-cost averaging. Reinvesting dividends is equally simple, allowing returns to compound over time without requiring manual action. This convenience makes mutual funds particularly attractive for beginners and long-term retirement savers who prefer a “set it and forget it” approach.

Advantages and Drawbacks

Mutual funds offer several advantages, including:

- Professional portfolio management

- Automatic diversification

- Easy recurring investments

- Wide selection of investment objectives

- Convenient dividend reinvestment

At the same time, investors should also consider potential drawbacks:

- Higher management fees than many ETFs

- Trading only once per day

- Potential capital gains distributions that may create taxable events

- Less flexibility for active traders

The right mutual fund can still be an excellent long-term investment, especially when it aligns with your financial objectives and risk tolerance.

What Is an Index Fund?

An index fund is designed to mirror the performance of a specific market index rather than attempting to outperform it. Instead of relying on a portfolio manager to actively select investments, index funds simply purchase the same securities found in their benchmark index, usually in the same proportions. This passive investment strategy has gained tremendous popularity because it reduces management costs while providing broad market exposure. Investors who choose index funds are essentially betting that, over time, the overall market will continue to grow, allowing them to participate in that long-term appreciation without trying to predict short-term winners and losers.

One important point that often confuses beginners is that an index fund is not necessarily a completely separate investment category. An index fund can exist as either a mutual fund or an ETF. For example, one company may offer an S&P 500 Index Mutual Fund, while another offers an S&P 500 ETF. Both track the same benchmark but differ in how investors buy, sell, and manage their investments. This is one reason the debate around ETF vs mutual fund vs index fund can become confusing, as the categories sometimes overlap rather than compete directly.

Passive Investing Explained

Passive investing focuses on matching market performance instead of beating it. This strategy reduces trading activity, lowers operating costs, and minimizes emotional investment decisions. Rather than reacting to every market headline or economic event, passive investors remain invested through market cycles and allow compound growth to work over decades.

The philosophy behind passive investing is surprisingly simple. Markets have historically trended upward over long periods despite experiencing short-term volatility. Instead of trying to predict every rise and fall, passive investors accept temporary declines while remaining focused on long-term wealth accumulation. Numerous academic studies have shown that this disciplined approach often outperforms frequent trading over extended investment horizons.

Why Index Funds Are So Popular

Several factors have contributed to the explosive growth of index funds:

- Very low expense ratios

- Broad diversification

- Reduced portfolio turnover

- Simple long-term investment strategy

- Consistent performance relative to market indexes

- Ideal for retirement investing

These advantages have made index funds one of the most recommended investment options for beginners, financial planners, and long-term investors alike.

ETF vs Mutual Fund vs Index Fund – Key Differences

Although these investment vehicles share many similarities, understanding their differences helps investors choose the option that best supports their financial goals.

Management Style

ETFs are often passively managed, although actively managed ETFs have become increasingly common. Mutual funds can be actively managed or passively managed, depending on the fund’s objective. Index funds are always designed to follow a market benchmark, making them passive by definition. Investors seeking professional stock selection may lean toward actively managed mutual funds, while those looking for market-matching returns often prefer index funds or passive ETFs.

Trading Flexibility

One of the biggest distinctions involves how investors buy and sell shares. ETFs trade continuously throughout market hours, allowing investors to respond to market movements in real time. Mutual funds, on the other hand, process purchases and redemptions only once each trading day after markets close. Index funds follow whichever structure they are built upon. If an index fund is structured as an ETF, it trades throughout the day; if it is structured as a mutual fund, it is priced only once daily.

Fees and Expenses

Investment costs may appear small initially, but they can significantly affect long-term returns due to compounding. Generally:

- ETFs often have the lowest ongoing expenses.

- Index mutual funds also maintain very low fees.

- Actively managed mutual funds usually charge higher expense ratios because of research and active portfolio management.

Even a small annual fee difference can result in thousands of dollars over decades, making cost an important consideration for long-term investors.

Tax Efficiency

Tax treatment varies depending on your country and account type, but ETFs are often considered more tax-efficient because of their creation and redemption mechanism, which may reduce taxable capital gain distributions. Mutual funds may distribute capital gains more frequently, especially when managers actively trade securities. Investors using tax-advantaged retirement accounts may not notice these differences immediately, but taxable account holders should carefully evaluate potential tax implications before investing.

Risk and Diversification

All three investment types provide diversification by spreading investments across multiple securities. Diversification helps reduce the impact of poor performance from any single company. However, diversification does not eliminate market risk. During major market downturns, even diversified funds may decline in value. The key advantage is that diversified portfolios generally recover more consistently over long investment periods than concentrated individual stock holdings.

Which Investment Is Best for Different Investors?

Choosing between ETF vs mutual fund vs index fund ultimately depends on your financial goals, investing style, and time horizon. There is no universal winner because every investor has unique priorities. Some people value flexibility and low costs, while others prefer professional guidance and automated investing. Before making a decision, consider how much time you want to spend managing your portfolio, how comfortable you are with market fluctuations, and whether you’re investing for retirement, wealth creation, or short-term financial goals.

A good investment strategy starts with understanding yourself rather than chasing market trends. Investors who constantly switch between investment products based on recent performance often achieve poorer results than those who stick with a disciplined plan. Think of investing like planting a tree—you don’t dig it up every few weeks to check the roots. Instead, you water it consistently and give it time to grow. The same principle applies to diversified investment funds. Patience, consistency, and low costs often matter far more than trying to find the “perfect” fund.

For Beginners

If you’re just starting your investment journey, simplicity should be your priority. New investors often feel overwhelmed by stock analysis, economic news, and market volatility. A diversified index fund or broad-market ETF allows you to participate in market growth without needing to research hundreds of individual companies.

Beginners should focus on:

- Building consistent investing habits

- Keeping investment costs low

- Diversifying across many companies

- Investing regularly regardless of market conditions

- Avoiding emotional buying and selling

Many financial professionals recommend starting with a low-cost index fund or ETF because these products provide broad exposure while minimizing expenses.

For Long-Term Investors

Long-term investors benefit most from the power of compound growth. Whether you’re saving for retirement, a child’s education, or financial independence, remaining invested for decades usually produces better outcomes than attempting to time the market. Index funds and ETFs are particularly attractive because their lower expense ratios allow more of your investment returns to remain in your portfolio.

Investors with long investment horizons should prioritize consistency over excitement. Market downturns are inevitable, but history has repeatedly shown that diversified portfolios have recovered over time. Regular contributions, dividend reinvestment, and patience often produce stronger long-term returns than frequent trading.

For Active Traders

Investors who actively monitor the market may prefer ETFs because they trade throughout the day just like individual stocks. This flexibility allows traders to react quickly to earnings reports, economic announcements, or changes in market sentiment. ETFs also support advanced trading strategies such as limit orders and stop-loss orders, which are unavailable with traditional mutual funds.

However, frequent trading comes with its own risks. Emotional decisions, higher transaction costs, and attempting to predict short-term market movements can reduce overall returns. Even active traders should ensure their investment strategy aligns with their financial goals rather than reacting impulsively to market headlines.

Common Mistakes to Avoid

Even the best investment product cannot guarantee success if poor investing habits undermine long-term performance. Many investors unknowingly make mistakes that reduce returns or increase unnecessary risk. Fortunately, these errors are often easy to avoid with a disciplined approach and a clear investment plan.

Some of the most common mistakes include:

- Choosing investments based only on recent performance

- Ignoring expense ratios and management fees

- Trying to time the market

- Failing to diversify across asset classes

- Selling investments during temporary market declines

- Investing without clear financial goals

- Making emotional decisions driven by fear or excitement

Successful investing is rarely about making perfect decisions every time. Instead, it’s about making consistently good decisions over many years. Staying invested, maintaining diversification, and avoiding emotional reactions often contribute more to wealth creation than constantly searching for the next high-performing fund.

Final Verdict

When comparing ETF vs mutual fund vs index fund, the best choice depends on what matters most to you as an investor. ETFs offer flexibility, lower costs, and tax efficiency, making them attractive for many modern investors. Mutual funds provide professional management, automatic investing, and convenience, particularly for retirement planning and employer-sponsored investment accounts. Index funds, whether structured as ETFs or mutual funds, emphasize passive investing, broad diversification, and long-term wealth accumulation through low-cost market exposure.

Rather than asking which investment is universally better, consider which one fits your personal investing style. A young investor building a retirement portfolio may prioritize low fees and choose an index ETF. Someone who prefers professional management and automatic monthly contributions may find actively managed mutual funds more suitable. In many cases, experienced investors even combine all three within a diversified portfolio to achieve different financial objectives. The most important decision isn’t selecting the “perfect” investment product—it’s developing a consistent strategy and sticking with it through changing market conditions.

Conclusion

Understanding the differences between ETF vs mutual fund vs index fund gives you the confidence to make smarter investment decisions. Although these investment vehicles share the common goal of diversification, they differ significantly in trading flexibility, management style, expenses, and tax treatment. Choosing the right one depends on your experience level, investment goals, and willingness to actively manage your portfolio.

For most investors, the key to long-term success isn’t finding a magical investment that outperforms every year. It’s maintaining a diversified portfolio, minimizing unnecessary costs, investing consistently, and allowing compound growth to work over time. Whether you select an ETF, a mutual fund, or an index fund, building disciplined investing habits will have a far greater impact on your financial future than chasing short-term market trends. Start with a clear plan, stay patient during market fluctuations, and remember that successful investing is a marathon—not a sprint.

Frequently Asked Questions

1. What is the main difference between an ETF and a mutual fund?

The primary difference is how they trade. ETFs trade throughout the day on stock exchanges like individual stocks, while mutual funds are priced and traded only once each trading day after the market closes.

2. Is an index fund the same as an ETF?

No. An index fund is an investment strategy that tracks a market index. It can be structured either as a mutual fund or as an ETF.

3. Which investment has lower fees?

In general, ETFs and index funds tend to have lower expense ratios than actively managed mutual funds because they require less active portfolio management.

4. Are ETFs better for beginners?

They can be. Broad-market ETFs offer diversification, low costs, and simplicity. However, beginners who prefer automatic investing may also find index mutual funds to be an excellent choice.

5. Can I invest in both ETFs and mutual funds?

Yes. Many investors build diversified portfolios that include both ETFs and mutual funds to balance flexibility, professional management, and long-term investment objectives.